Fantastic lecture by Bill Dally (NVIDIA) on Deep Learning Hardware.

With one clear lesson: DEEP LEARNING WAS ENABLED BY HARDWARE.

The theory and the algorithms were known since few decades, but deep learning only started to work when computing hardware became sufficiently advanced to enable the training of a complex network in a reasonable time (the famous AlexNet paper).

Second lesson: hardware is not enough. A properly optimized software stack can lead to performance improvements of orders of magnitude.

In graduate engineering lectures, we mainly focus on the technical, physical, and system-level aspects of the different issues, rarely broadening the view to the global economic or industrial scenario.

But in recent times semiconductors (and the geopolitics of semiconductors) are often in the News, so I decided to dedicate to the topic some time in class last week.

This is a surprising graph: it is the 2020 production of chips (in total area of silicon dies [1]) subdivided by country or geographic area of fab location e type of technology. Technology is expressed as a number of nanometers, which indicate an equivalent scale factor [2].

Today, the most advanced available technology is the “5 nanometers” (5 nm), available only in Taiwan (TSMC) and in South Korea (Samsung), maybe soon in the US (Intel). In the graph, it is indicated in red (“< 10 nm”): it is the technology required for advanced processors for smartphones (Apple, Qualcomm), laptops, game consoles (Sony, Microsoft), advanced graphics (Nvidia). Europe, China, and the USA do not have this technology and must buy from Taiwan and Korea. The US is trying to be back in the game and to keep China out. European countries are only hoping that a big company from abroad builds a fab.

For this technology, there is a global production scarcity, as everybody trying to buy a PS5 PlayStation in the last year has noticed. Why: a single fab has a cost of 1-20 B$, years to have it in operation, with great risks associated to technology, infrastructures, and market.

The technology used of chips in cars and advanced mechanical equipment is mostly from 40 nanometers and up, a set of technologies introduced between 10 and 20 years ago. They are the orange and blue bars in the graph. They are relevant in Europe and in the whole world, because they require smaller CAPEX (< 1 B$) and are old, and because the main customers (the Auto and Mechanics Industry) are in Europe.

Also chips fabricated with these mature technologies are scarce: we all have read the news of carmakers that have reduced car production because chips are not available. How is it possible? Because too many are increasing inventory, I am afraid, in order not to find themselves without chips the next time. Basically, the same mechanisms according to which toilet paper disappeared from supermarkets at the beginning of the pandemic. It is not a structural scarcity, just a panic moment, we need to wait that the inventory is full.

I do not want to add anymore because the post is already too long, but there is a lot more. The semiconductor sector is hot from the scientific point of view, from the technological point of view, and from the points of view of economics and politics.

As usual, the feeling is that TV and politics use slogans and do not have a clear picture of the issues (and I fall again in Gell-Mann amnesia [3]).

[1] The unit of measure of the plot is a wafer – a thin silicon pizza – with a diameter of 200 mm on which hundred or thousands of chips are fabricated.

[2] Up to 15 years ago the name of the technology node used to indicate the main transistor length (the gate length), but now is only a scale factor: the number of transistors per centimeter squared of silicon is inversely proportional to the scale factor (therefore, for example, the “10 nm” technology contains four times the number of transistor per square cm than the “20 nm” technology).

A conversation with Yanis Varoufakis on his vision for an alternative world, beyond the present version of capitalism – that he calls technofeudalism – presented in his new book, Another Now; Dispatches from an Alternative Present.

Yanis Varoufakis has been Finance Minister of Greece in 2015 at the time of the Greek debt crisis, is Member of the Hellenic Parliament, founder of the transnational Democracy in Europe Movement 2025 (DiEM25), co-founder of the Progressive International organization. He is Professor of Economics at the University of Athens, has a MS in mathematical statistics from Birmingham University and a PhD in Economics from the University of Essex.

Yanis Varoufakis is one of the leading public intellectuals with worldwide recognition and we are really honored he accepted to have a public conversation on the issues discussed in his new book.

Another Now is a fascinating book. It is a science fiction novel, in which he uses as a literary device the “many-world” theory to describe another world in which his vision of a market economy without capitalism has come to existence, following an alternative history that departed from our world in 2008, during the financial crisis.

This device gives him the possibility to describe the details of the organization of this “Another Now”. Personally, I could identify with Kosta, the technologist, one of the novel’s protagonists.

I21 is a series of conversations with Giuseppe Iannaccone on how to prepare for the future, and the impact of technology and science on society, jobs, culture, economics, education. The playlist of i21 is here: https://www.youtube.com/playlist…

This conversation is part of the EVO4.0 research project, partly funded by the POR FESR Tuscany Region 2014-2020 (Action 1.1.4 sub b) within the Crosslab IT& Society of the Departiment of Information Engineering, Università di Pisa.

The basic premise of the quantum reconstruction game is summed up by the joke about the driver who, lost in rural Ireland, asks a passer-by how to get to Dublin. “I wouldn’t start from here,” comes the reply.

Where, in quantum mechanics, is “here”? The theory arose out of attempts to understand how atoms and molecules interact with light and other radiation, phenomena that classical physics couldn’t explain. Quantum theory was empirically motivated, and its rules were simply ones that seemed to fit what was observed. It uses mathematical formulas that, while tried and trusted, were essentially pulled out of a hat by the pioneers of the theory in the early 20th century.

Quantum mechanics is at the basis of the operation of solid-state electronics and optoelectronics, and therefore enables the whole ICT and Internet world.

However, it is still introduced to students as a new science, a revolution with respect to “classical” science, and as something that is basically strange and unintuitive. This is because the historical view of the birth of quantum mechanics is still dominant, after all these years. So all new attempts at rebuilding the foundations of quantum physics are welcome (and I admit I still very much like David Bohm’s view).

Again on the topic of too few new tech companies in Europe, and especially in Italy.

The Atomico report on the “State of European Tech 2017” shows a list of all tech companies, either private, public, or acquired funded since 2003 with a valuation higher than one billion dollars.

The total number is 41:

16 are private

16 are public

9 have been acquired.

The breakdown per country is familiar:

13 UK

7 Germany

6 Sweden

3 France

3 Russia

2 Finland

2 Denmark

2 Netherland

1 Ireland

1 Slovenia

1 Switzerland

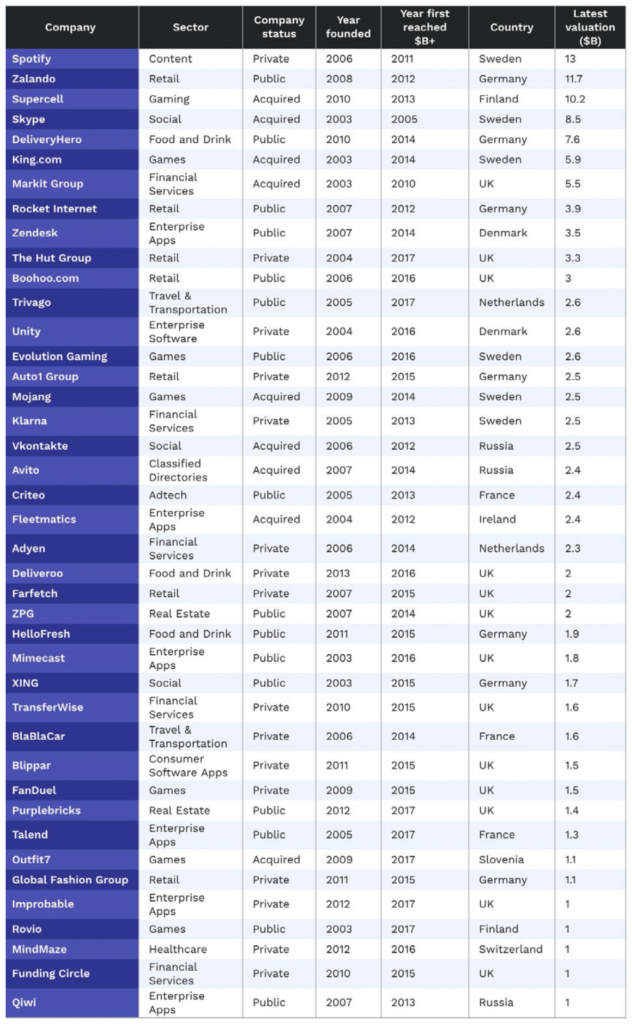

A quick look at the private companies with a valuation in excess of 1 billion dollars backed by venture capital (the so-called “unicorns”) shows that very few come from Europe (and none from Italy). They are not yet real valuations, but they can be a good proxy in terms of continent or country share.

These data are taken from the dedicated page on the WSJ website, considering valuations in January 2018.

103 companies from the US

46 from Asia (which means mostly China, then India)

15 from Europe

6 from Other (Canada, Australia, Africa)

As a breakdown of the 15 companies from Europe we have:

6 from the UK (Oxford Nanopore, Farfetch, TransferWise, Deliveroo, Shazam, Funding Circle)

3 from Germany (Auto1Group, HelloFresh, CureVac)

2 from Sweden (Spotify, Klarna)

1 from The Netherlands (Adyen)

1 from France (BlaBlaCar)

1 from Luxembourg (Global Fashion Group)

1 from Czech Republic (Avast Software)

Then only 1 from Israel (IronSource) as of today.

One can discuss the reasons for this distribution, but I do not have a simple answer and have to look at some more data.

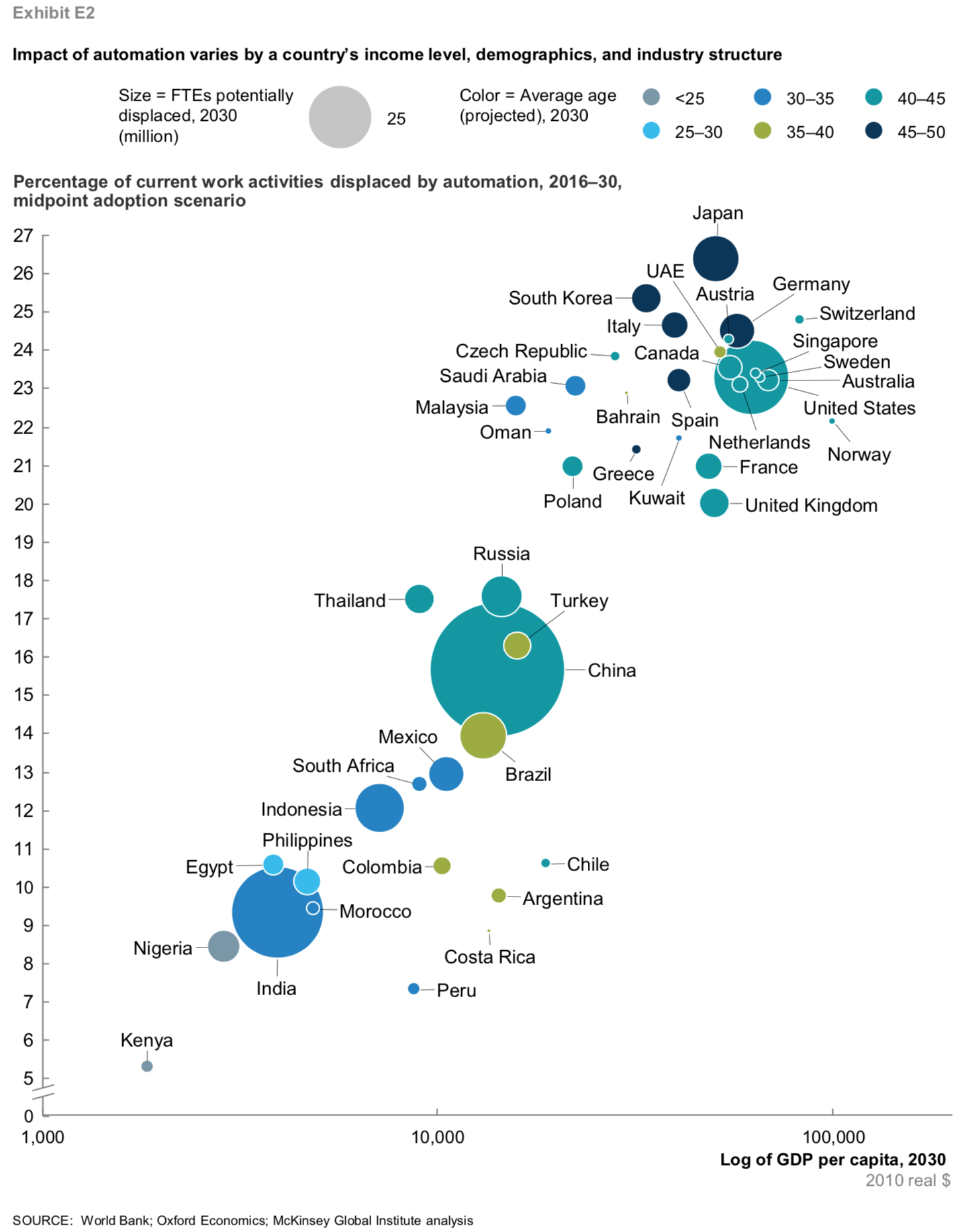

This figure is self-explanatory and is taken from the December 2017 McKinsey Global Institute report Jobs lost, jobs gained: Workforce transitions in a time of automation. The main prediction is that between 20% and 27% of work activities (measured in units of time) will be displaced due to automation in 2030 in advanced economies. Countries with an aging population will be affected the most. This is only one part of the equation. The other (missing) part is the number of new jobs, in order to understand whether they will be able to offset the displaced jobs. Nobody knows the answer because it depends on the structure and the choices of institutions.

I love listening to podcasts while driving, running, or doing chores. Here I just want to share a few links to some recent episodes I really enjoyed.

Season 2 of Malcolm Gladwell’s podcast Revisionist History is fantastic. The Basement Tapes is one of my preferred episodes [link]. Deep, thoughtful, surprising, and perfectly done. At the level of some of the best stories in The Tipping Point [link]

Episodes 14 and 15 of Reed Hoffman’s Masters of Scale podcast, with a long interview with Barry Diller [link].

The Ezra Klein long interview with Paul Krugman on politics, Trump, incentives [link]

Episode 131 of the Exponent Podcast [link] where Ben Thompson and James Allworth discuss disruption and the critical differences between today’s world and the scenario discussed in Clayton Christensen’s classic book The Innovator’s Dilemma [link]

This is the critical difference between the IT-era and the Internet revolution: the first made existing companies more efficient, the second, primarily by making distribution free, destroyed those same companies’ business models.

The important insight is that in a first phase the widespread use of IT increased productivity and earnings, by streamlining production. But only when IT and Internet streamlined distribution, incumbent companies crumbled down.

Many markets have been completely destroyed and re-built (on a smaller scale) by Internet giants and newcomers.

The newspaper business is a shadow of what it used to be. So are travel agencies and directory companies. Their business model, i.e. the capability to get paid, was enabled by owning distribution (not the mithical means of production).

What will the next step be? My hunch is that it could be “accreditation”. Then it is going to be hard for the Education and Health sectors.

Again, this is a good opportunity for existing Universities and Schools, for Health Companies and Hospitals, to move first.

But it also a good opportunity for newspapers to play a new game.